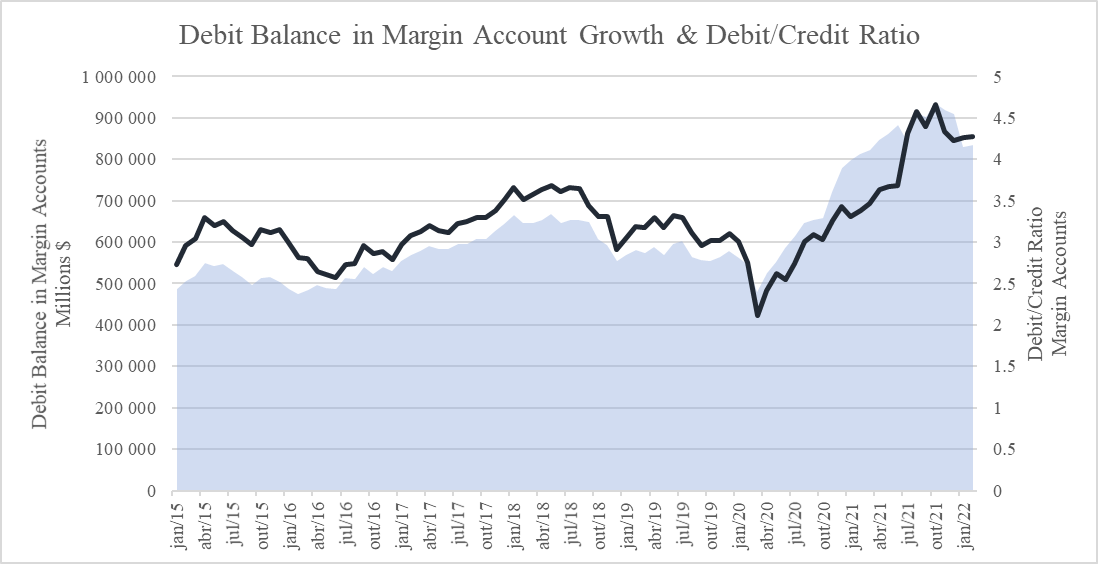

In today’s world, of extremely low interest rates across the board, the amount of leverage in the system has been increasing substantially. As expected, Investors & Speculators have been using low interest rate debt in order to increase returns and leverage their investments - as we can see below, debit balances in margin accounts are close to a record high - peaking around 900 Bln $ in 2022 - with debit to credit ratios hitting ~4.6x.

Consequently, there is an increasing sensitivity to interest rate changes in the system and as previously studied, the simultaneous unwinding of leveraged positions can trigger financial market turbulence.

However, looking at outstanding margin loans does not paint the full picture regarding the amount of leverage in financial markets. Although balance-sheet measures of leverage are available, it is useful to take into consideration measures of leverage that incorporates both on- and off-balance-sheet activities.

Since the introduction of the Dodd–Frank Wall Street Reform and Consumer Protection Act in July 2010, a significant portion of derivative contracts that were being traded in the OTC markets moved to exchanges and thus enhancing the process of price discovery and ensuring the optimal level of margining and collateral exchange by market participants significantly reducing the chances of counterparties building up large uncollateralized losses.

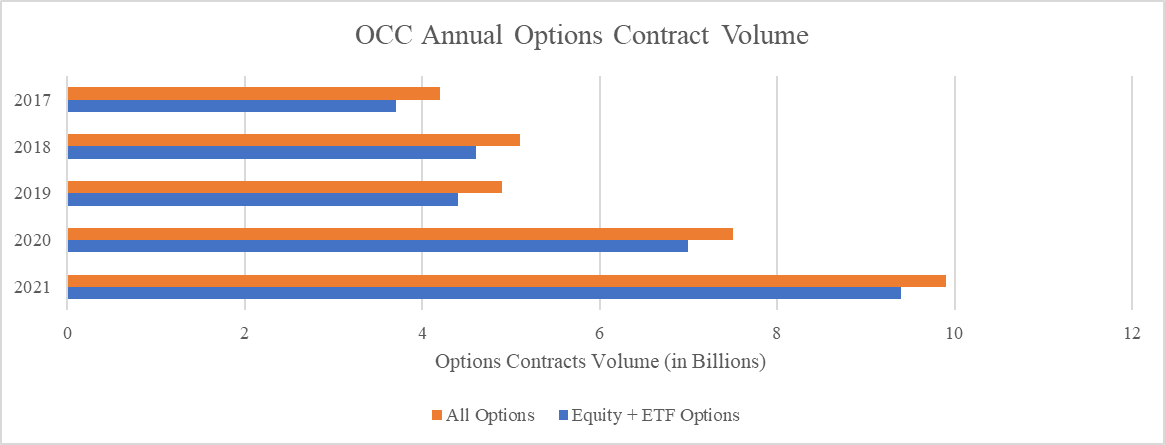

With the commoditization of standardized derivatives such as Options and Futures, retail adoption of derivatives trading skyrocketed after 2018 on the heels of brokers like Robinhood - introducing, among other things, free trading, easy sign ups, easy access to options, referrals and a simplified UI.

Since then, several brokers and exchanges have been reporting substantial growth in Options ADV. The OCC has also been reporting several records of Option Volume and Open Interest over the last couple of years. This year the US options market is already off to a strong start with an average daily volume near 43.4 million contracts, suggesting that a total near 11B contracts may be achieved this year, after record-breaking performance in 2021 and 2020.

Now that we have established how popular standardized options have become in recent years, associated with the leverage it provides, virtually no counterparty risk and the amount of liquidity that these markets draw in today’s world we may move forward in our explanation of why unusual activity matters.

In a digital information era, information transfers have become more and more frictionless. Consequently, the propension associated with data leaks is also increasing substantially over the last decade.

The concept of Asymmetric Information is at the core of ZackFinds.com value proposition. It refers to a situation when one party in a transaction is in possession of more information than the other. In certain transactions, sellers can take advantage of buyers because asymmetric information exists whereby the seller has more knowledge of the asset being sold than the buyer. The reverse can also be true.

But before we delve into unusual options linked to asymmetric information we will write, in the next part of this series, about the implications of the options market in the underlying stock price action. As the derivatives grow exponentially the propension to manipulate it is also expected to grow - some abusive behaviors have been reported by the SEC since 1973 with some being classified, at the time, as “mini manipulation”.

Subscribe for Part 2

ZackFinds.com

Follow the Smart Money