Unusual Option Activity - Why it Matters? Manipulation Concerns

Part 2

In the Part 1 of “Why Unusual Activity Matters” we wrote about the increasing amount of leverage in the system - on- and off balance sheet leverage. In particularly we focused on the recent meteoric growth of Options Trading.

In this post we will go back to 1973 - The year where Fischer Black and Myron Scholes finally published an article titled "The Pricing of Options and Corporate Liabilities". That same year Chicago Board Options Exchange (Cboe) is founded and becomes the first marketplace for trading listed options.

In 1977, due to the explosive growth of the options market, the SEC decided to conduct a complete review of the structure and regulatory practices of all option exchanges - this studied was called the “Special Study of the Options Markets” and published in late 1978.

The study pointed out several abuses by market participants - and the lack of resources to monitor complex trades. Additionally, the SEC also pointed out a type of behavior that was at the time classified as “mini-manipulation”.

“Affecting stock transactions to depress or prevent a rise in the price of a stock in order to prevent near the money, at-the-money, or slightly in the money call options from being exercised, and to protect a previously received premium, is referred to as capping.

Similarly, affecting stock transactions to prevent a decline in the price of a stock, in order to assure that put options written on the stock will not be exercised and that premiums previously received will be protected is referred to as pegging.”“(…) These practices are most likely to occur just before expiration of the options series, when the probability of exercise is highest. Capping and pegging are forms of minimanipulation.”

Special Study of the Options Markets, SEC December 1978

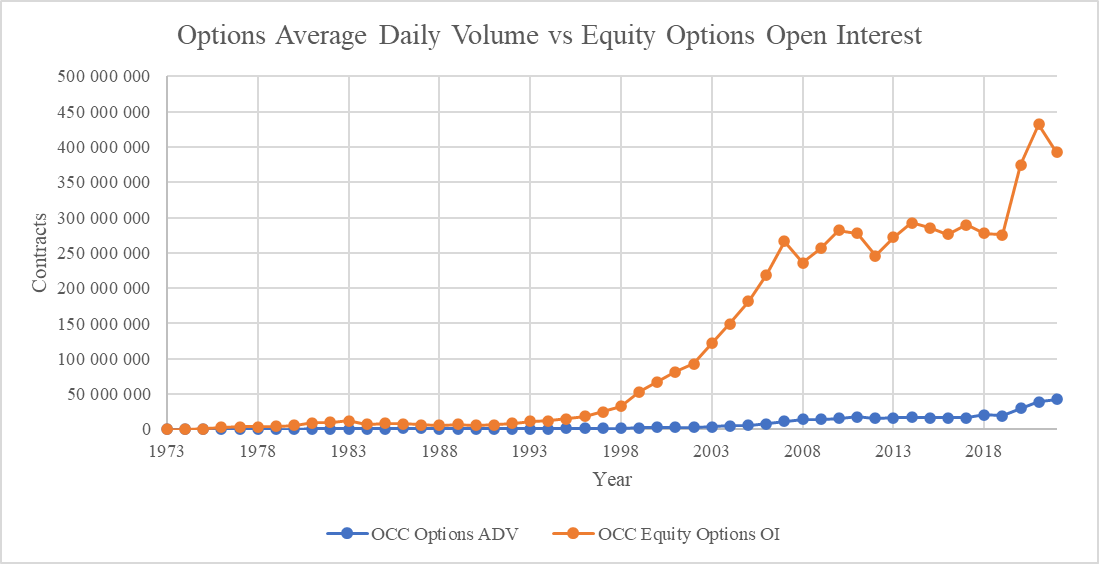

It is important to mention that, in relative terms, the options market grew ~6,640x in terms of contract ADV - from around 6,400 contracts in 1973 to 42.5 Million in 20221. Recently, single-day total volume record was broken twice on two consecutive trading days: on Friday, January 21 2022 with 63.5 million contracts and Monday, January 24 2022 with 63.7 million contracts.

Since 1978, some studies have been developed to try and understand why mini-manipulation happens and if this kind of behavior is still present in the markets. Most of the research attributes pinning events to Dynamics Hedging. In the other hand, over the years some cases of mini-manipulation have been brought up by the SEC against multiple institutional market participants.

Additionally, the studies focusing on stock pinning at strike prices on OpEx trading days vs non-OpEx trading days seem to show that “mini-manipulation” events are still present in the market - and that these are solely the tail of the cat. Ignoring that the options market is getting too big too fast and that the implications in the underlying market are negligible might not be the best idea.

More recently, Gene DeMaio currently Executive Vice President in FINRA's Market Regulation Department, with the responsibility for managing the Options Regulation and Trading and Financial Compliance Examinations programs - stated the following on Mini-Manipulation:

“It was first discussed as far back as the 1978 Securities and Exchange Commission report on options,”

“It never really got much play after that because there were not many violations that we uncovered for years, and years, and years.”

However, as surveillance tools have been evolving, FINRA is receiving an increasing number of mini-manipulation alerts in both illiquid and extremely liquid stocks. They also found different types of mini manipulation, including spoofing the option after manipulating the equity price in an attempt to move the option’s price further.

In the chart below we can see the average percentage of optionable stocks pinning at a strike price around monthly OpEx cycles from 2010 to 2015.

It does seem odd that during OpEx expirations the amount of pinning events experience an abnormal increase. However, once again, this is only the tail of a cat - exposed by a relatively simple analysis.

Once we understand that the exponential rise of Options Trading is indeed affecting price discovery and the underlying asset supply-demand dynamics we start to take into consideration hedging flows and the impact of the notorious Vanna & Charm flows that some twitter users have been expressing over the last couple of years.

Subscribe for Part 3

ZackFinds.com

Follow the Smart Money

According to the Options Clearing Corporation latest report - https://www.theocc.com/Newsroom/Press-Releases/2022/02-02-OCC-January-2022-Total-Volume-Becomes-Highes